2 R Playgrounds

2.1 Expected Value and Standard Deviation

Roulette table example with Red, Black and Green. Only Green wins. Whats the probability that you get Green?

v = rep(c("Red", "Black", "Green"), c(18,18,2))

prop.table(table(v))## v

## Black Green Red

## 0.47368421 0.05263158 0.47368421This is the sampling model.

x = sample(c(17,-1), prob = c(2/38,36/38))The expected value is calculated by adding the possible value times their likelyhood together. Its formula is ap + b(1-p). The expected value for 1000 draws.

EV = 1000 * (17*2/38 + (-1*36/38))The standard error (standard deviation of random variables i.e., probability distributions). Its formula is a - b * sqrt(p * (1-p)). The standard error for 1000 draws.

SE = sqrt(1000) * (-((-1)-17) * sqrt(2/38 * 36/38))Random variable S storing the experimental values from sampling model.

set.seed(1)

S = sample(c(17,-1), size = 1000, replace = T, prob = c(2/38, 36/38))

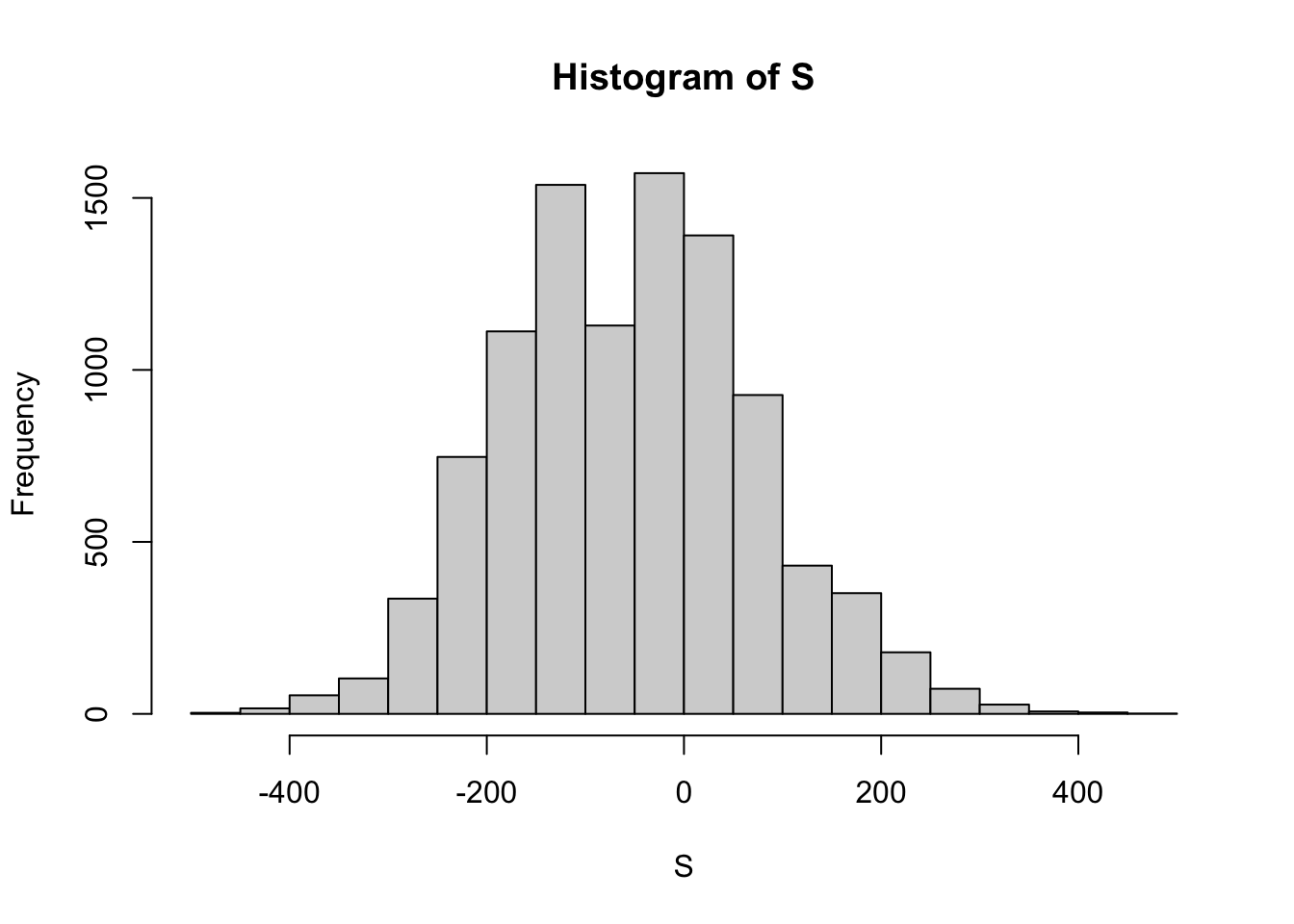

sum(S)## [1] -10Create the experimental sampling distribution of the sample sum.

roulette_winnings = function(){

S = sample(c(17,-1), size = 1000, replace = T, prob = c(2/38, 36/38))

sum(S)

}

set.seed(1)

S = replicate(10000, roulette_winnings())

hist(S)

The mean or expected value of X?

mean(S)## [1] -52.3324The standard deviation or standard error of X?

sd(S)## [1] 126.9762The probabilty that we win?

mean(S > 0)## [1] 0.3391n = 1000

pbinom(500, size = 1000, prob = 1/19) # ??## [1] 12.2 Theoretical and Experimental Standard Error

The sample statistics: 0.45 “democrats and a sample size of 100.

p = 0.45

n = 100The theoretical standard error for p = 0.45 and sample size n = 100.

SE = sqrt(p * (1 - p)) / sqrt(n)

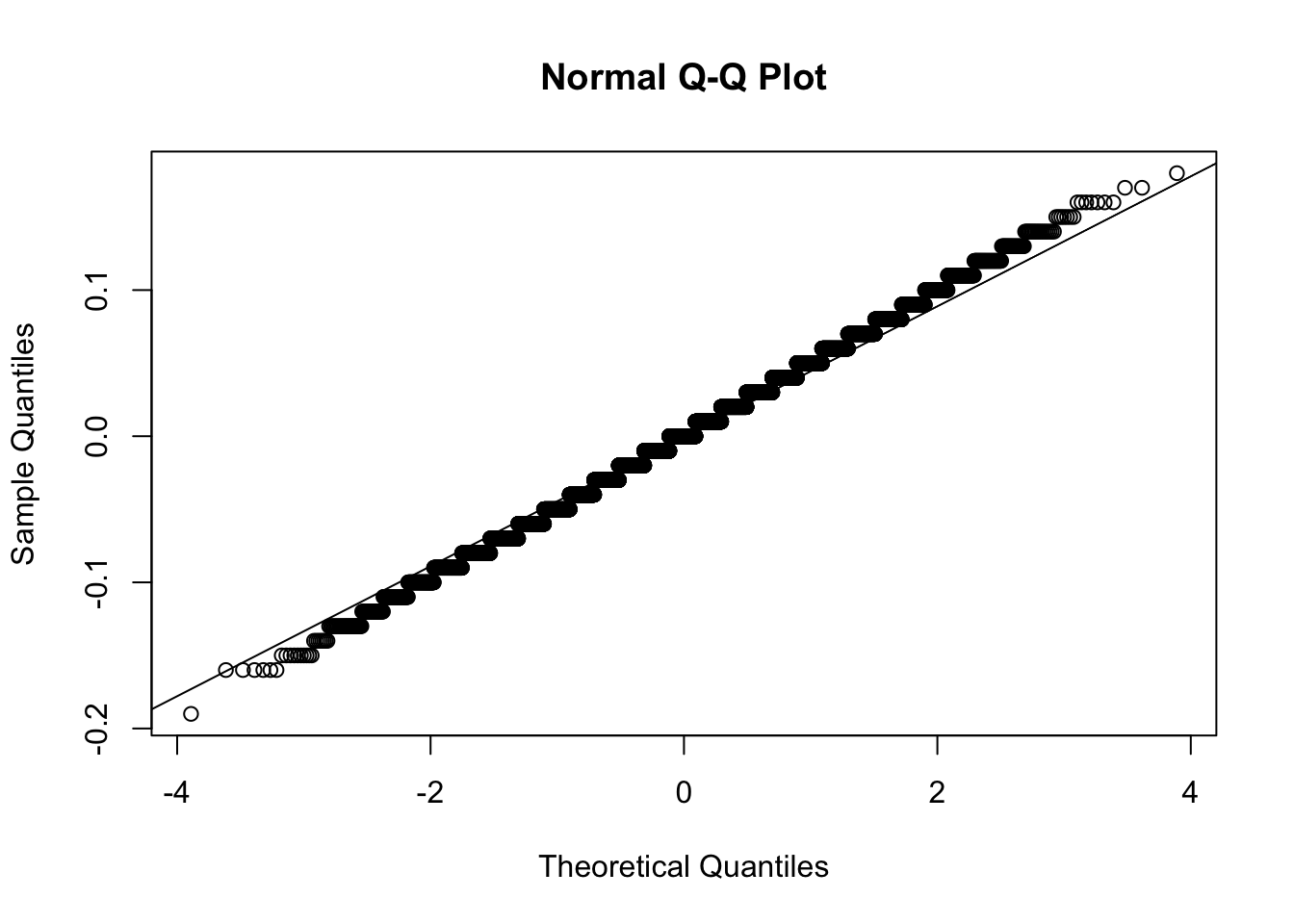

SE## [1] 0.04974937Now we can experimentally proof this expected standard error by running a Monte Carlo simulation. We basically create a sampling distribution of size 10000 of the sample proportions with p = 0.45 and n = 100. Only that we lastly subtract p to find out the actual error.

test_errors = replicate(10000, mean(sample(c(1,0), replace = T, size = n, prob = c(p, (1 - p)))))

# Distribituon of errors

test_errors = test_errors - p

# The standard deviation of the errors

sd(test_errors)## [1] 0.04960875# Very close to the theoretical standard error

SE## [1] 0.04974937And the error distribution is approximatly normal.

qqnorm(test_errors);qqline(test_errors)

2.3 Sample Size Resulting in 0.01 SE

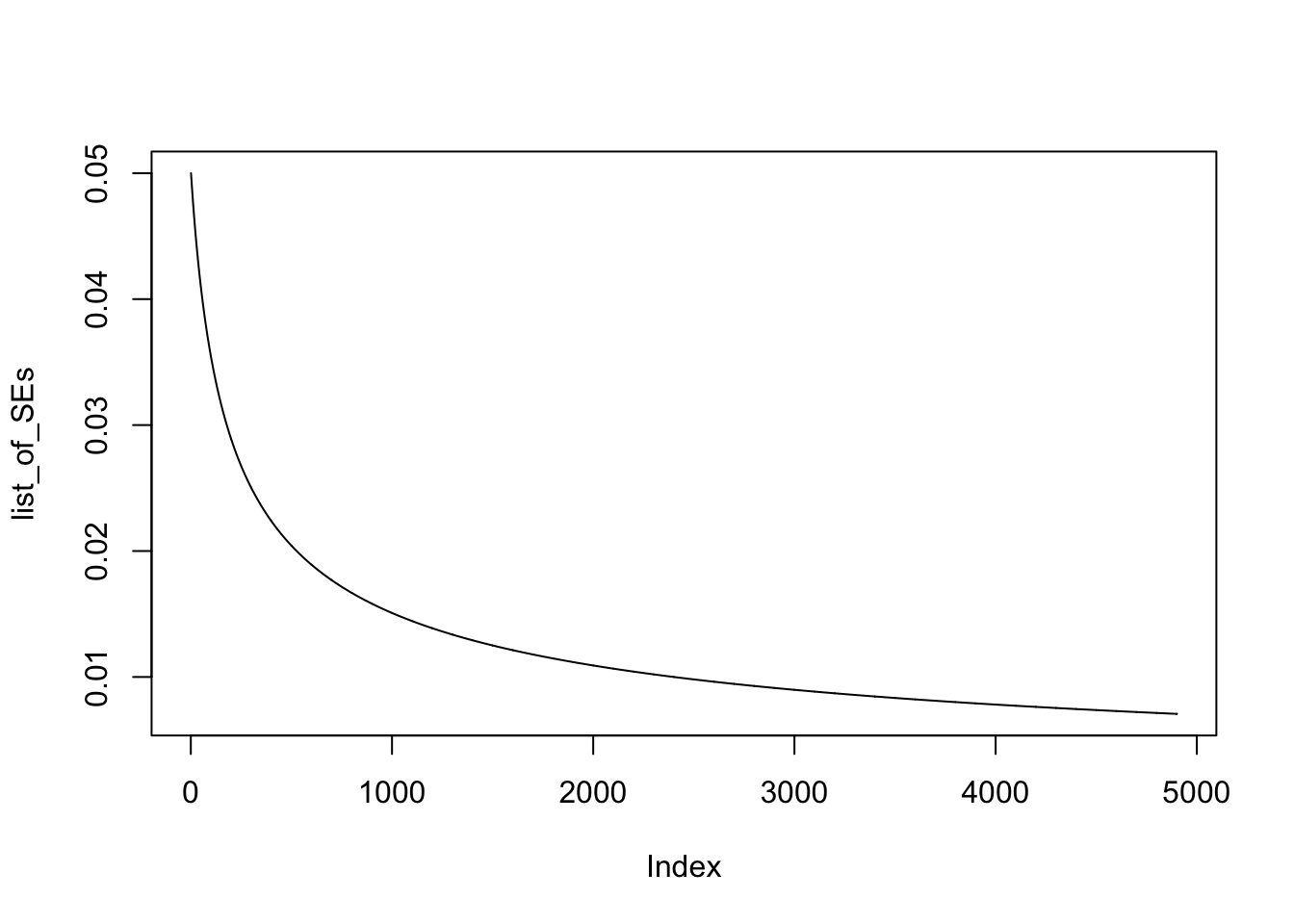

The maximum SE in relation to proportions is with p = 0.5. Therefore we will take this worst case scenario case to calculate our goal, the required sample size to get a standard error arround 0.01. We can calculate a list of SE based on sample sizes 100 to 5000.

p = 0.5

n = 100:5000

list_of_SEs = sqrt(p * (1 - p) / n)

head(list_of_SEs, 20)## [1] 0.05000000 0.04975186 0.04950738 0.04926646 0.04902903 0.04879500

## [7] 0.04856429 0.04833682 0.04811252 0.04789131 0.04767313 0.04745790

## [13] 0.04724556 0.04703604 0.04682929 0.04662524 0.04642383 0.04622502

## [19] 0.04602873 0.04583492When plotting the list of standard errors we can see at what sample size we will reach a standard error of around 0.01: with a sample size of around 2.500.

plot(list_of_SEs, type = "l")

2.4 Bank and Loans

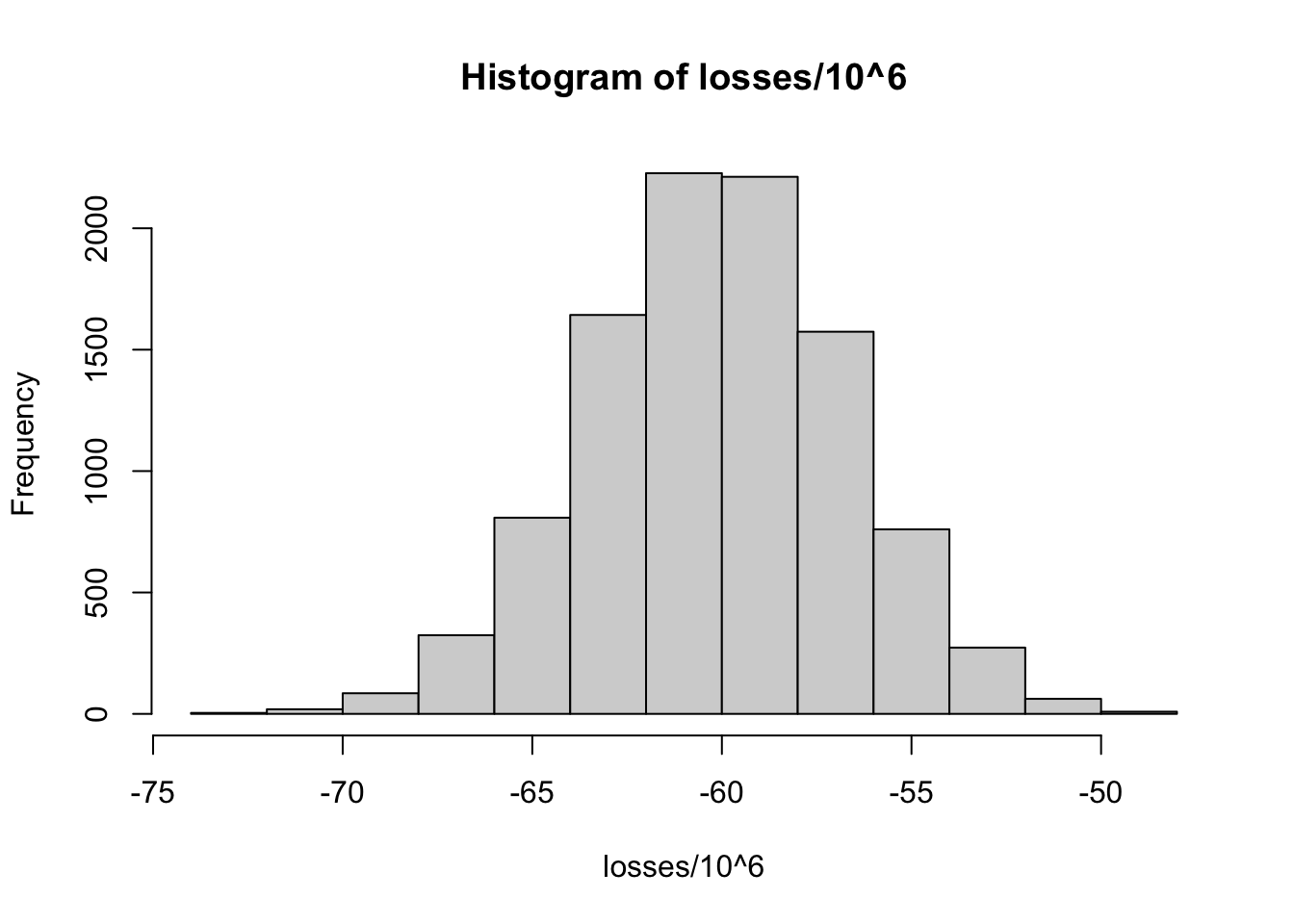

# Number of loans

n = 10000

# Probability of default

p = 0.03

# Loss per single forclosure

loss_per_forclosure = -200000

# Interest_rate

x = 0

# Random variable S storing defaults = 1 and non defaults = 0

S = sample(c(0,1), prob = c(1-p, p), size = n, replace = T)

head(S, 100)## [1] 0 0 0 0 0 0 0 0 0 0 0 0 1 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

## [38] 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 1 0

## [75] 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 1# Expected value for 10000 loans

sum(S * loss_per_forclosure)## [1] -62600000# Monte-Carlo simulation amount

B = 10000

# Simulation

losses = replicate(B, {

S = sample(c(0,1), prob = c(1-p, p), size = n, replace = T)

sum(S * loss_per_forclosure)

})

# Losses distribution from simulation

hist(losses / 10^6)

# Expected value of S

EV = x*(1-p) + loss_per_forclosure*p

EV## [1] -6000# Standard error of S

SE = abs(x - loss_per_forclosure) * sqrt(p * (1-p))

SE## [1] 34117.44# Loans of 180000

x = 180000

# loss_per_forclosure*p + x * (1-p) = 0

# Find out x!

x = - (loss_per_forclosure * p / (1 - p))

x## [1] 6185.567# Interest of 6185.57 dollars for each loan needed to get on average 0 in total back as the bank.

EV = loss_per_forclosure * p + x * (1 - p)

EV # Correct!## [1] 02.5 Real Polling Data

# library(dslabs)

data("polls_us_election_2016")

# Exclude observations that are too old.

polls <- polls_us_election_2016 %>%

filter(enddate >= "2016-10-31" & state == "U.S.")

head(polls, 5)## state startdate enddate pollster grade samplesize

## 1 U.S. 2016-11-03 2016-11-06 ABC News/Washington Post A+ 2220

## 2 U.S. 2016-11-01 2016-11-07 Google Consumer Surveys B 26574

## 3 U.S. 2016-11-02 2016-11-06 Ipsos A- 2195

## 4 U.S. 2016-11-04 2016-11-07 YouGov B 3677

## 5 U.S. 2016-11-03 2016-11-06 Gravis Marketing B- 16639

## population rawpoll_clinton rawpoll_trump rawpoll_johnson rawpoll_mcmullin

## 1 lv 47.00 43.00 4.00 NA

## 2 lv 38.03 35.69 5.46 NA

## 3 lv 42.00 39.00 6.00 NA

## 4 lv 45.00 41.00 5.00 NA

## 5 rv 47.00 43.00 3.00 NA

## adjpoll_clinton adjpoll_trump adjpoll_johnson adjpoll_mcmullin

## 1 45.20163 41.72430 4.626221 NA

## 2 43.34557 41.21439 5.175792 NA

## 3 42.02638 38.81620 6.844734 NA

## 4 45.65676 40.92004 6.069454 NA

## 5 46.84089 42.33184 3.726098 NAThe first poll. Create a confidence interval.

n = polls$samplesize[1]

x_hat = polls$rawpoll_clinton[1]/100

se_hat = sqrt(x_hat * (1 - x_hat) / n)

cf = c(x_hat - 1.96 * se_hat, x_hat + 1.96 * se_hat)

rm(x_hat, se_hat)Create columns for x_hat, se_hat, lower and upper confidence bounds. Select only the relevant columns.

polls = polls %>%

mutate(x_hat = polls$rawpoll_clinton/100,

se_hat = sqrt(x_hat * (1 - x_hat) / samplesize),

lower = x_hat - 1.96 * se_hat,

upper = x_hat + 1.96 * se_hat) %>%

select(pollster, enddate, x_hat, se_hat, lower, upper)Create a hit column indicating whether our confidence intervals included our true parameter, the final vote count for Clinton 48.2.

polls = polls %>%

mutate(hit = ifelse(0.482 > lower & 0.482 < upper, TRUE, FALSE))

mean(polls$hit)## [1] 0.3142857